The motor finance industry faces its first major remediation crisis in the AI era, driven by the now-banned practice of Discretionary Commission Arrangements (DCAs). Declared unlawful in October 2024, DCAs have triggered a surge of complaints, with the FCA’s findings due by May 2025.

The potential scale of this crisis is staggering. Over a million complaints were lodged in just 33 days in early 2024 through Money Saving Expert. Major banks such as Lloyds (£450 million) and Santander (£295 million) have already provisioned significant sums. Some experts predict this could rival the £50 billion cost of the PPI scandal, marking it as one of the most significant remediation challenges in UK banking history.

PPI's slow, manual processes led to significant reputational damage, operational strain, and years of prolonged remediation efforts. But this time, financial institutions have a powerful ally in AI.

AI offers a transformative opportunity to manage this challenge efficiently, reducing costs, safeguarding reputations, and even turning this crisis into a testbed for modernising operations. However, with mere months until regulatory deadlines, time is of the essence.

Learning the lessons of PPI failures

The PPI scandal became a byword for operational inefficiency and reputational fallout. Financial institutions relied on armies of temporary staff to manually process claims, which led to slow response times, inconsistent customer experiences, and billions of pounds in additional costs.

The parallels with DCAs are striking: fragmented data, regulatory scrutiny, and overwhelming customer demands. However, AI provides an opportunity to streamline the process – from data aggregation to claim triaging and resolution.

The stakes are high. The consequences of failing to address the motor finance remediation challenge quickly and effectively are severe, spanning reputational, operational, and regulatory risks.

Consumer trust in the banking sector is already fragile. Mishandling this issue risks worsening dissatisfaction, as cases like the Farage-Coutts controversy have shown how quickly public sentiment can spiral. Operationally, banks without scalable processes will face unsustainable costs, relying on temporary staff and diverting resources from core functions. This creates inefficiencies, prolongs resolutions, and increases the risk of errors – further damaging customer trust and attracting regulatory scrutiny.

Finally, the regulatory penalties for non-compliance are likely to be punitive. The FCA's Consumer Duty regulations require organisations to treat customers fairly, communicate clearly, and resolve issues promptly. Further, the FCA has made it clear that the use of AI and other technologies must align with their principles of fairness and consumer benefit, adding another layer of complexity to remediation efforts.

For financial institutions, this is clearly a challenge, but the smartest organisations will see it as an opportunity to demonstrate their commitment to customers and regulators while showcasing their ability to adapt to the demands of the AI era.

AI advantage: speed, scalability, and precision

In tackling the £50bn motor finance remediation challenge, AI offers a transformative solution that can revolutionise how financial institutions approach large-scale redress programmes. Unlike the manual, error-prone processes that characterised PPI remediation, today's AI technologies – such as Generative AI and Large Language Models – enable faster, more accurate, and scalable operations.

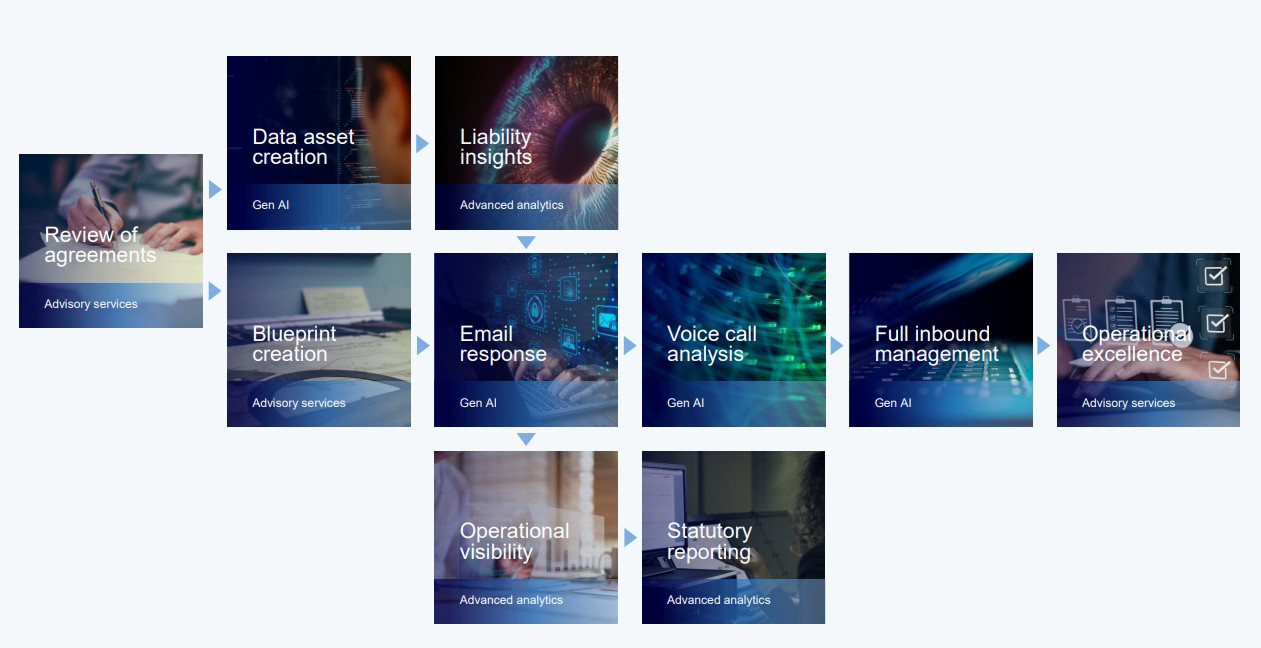

For many lenders, data fragmentation presents the first hurdle. Agreements dating back to 2007 form the basis of the remediation effort, but in many cases, lenders lack complete or centralised records. Historical agreements may be stored across multiple systems, unstructured data like scanned PDFs or even paper archives.

AI can address this by extracting, standardising, and validating data from disparate sources. For instance, gen AI can analyse unstructured content in old contracts, pulling out key details such as loan values, interest rates, and payment histories, and then consolidate this information into a comprehensive "data asset". This foundational dataset enables accurate assessments of customer eligibility for redress.

Once the data is prepared, AI accelerates the claims process. Traditional methods often require weeks – or even months – to review agreements, calculate redress amounts, and communicate decisions. By comparison, AI-powered systems can complete these tasks in hours.

For instance, LLMs can be trained to analyse agreements, identify discrepancies, and precisely calculate compensation amounts. They can then generate tailored responses for each customer, ensuring that communications are clear, consistent, and in line with FCA Consumer Duty regulations. This speed and accuracy translate into a huge reduction in resolution times – by as much as 70% – while improving transparency and customer satisfaction.

Customer communication is another area where AI shines. One of the most common complaints during PPI remediation was responses' inconsistent and impersonal nature. Many customers felt they were facing a faceless institution rather than being heard. AI-driven communication tools can provide a more personalised approach, offering multi-channel support across email, web portals, in-app messaging, and traditional letters. These tools ensure that every message is tailored to the customer's unique circumstances, fostering trust and demonstrating a commitment to fair treatment.

Finally, AI solutions offer unparalleled scalability. Traditional remediation efforts would require the hiring and training hundreds of temporary staff, a costly and inefficient approach. Conversely, AI can handle fluctuating claim volumes seamlessly, adapting to demand without compromising quality or compliance.

By consolidating fragmented data, streamlining claims processing, enhancing customer communication, and enabling scalability, AI provides financial institutions with the tools they need to meet the FCA's likely May 2025 deadline efficiently and effectively.

A test drive for AI

Beyond addressing the immediate motor finance challenge, AI-powered remediation programmes offer a unique opportunity for financial institutions to test and refine their AI capabilities. Unlike core banking products, motor finance represents a non-critical but high-value use case, making it an ideal proving ground for deploying AI at scale.

Successfully implementing AI-driven solutions in this context can give banks valuable insights and build confidence in the technology. This will pave the way for broader adoption across operations. The same principles and technologies could benefit areas such as fraud detection, regulatory compliance, and customer service.

This is also an opportunity for financial institutions to shift their approach to regulatory challenges. Instead of viewing compliance as a burden, forward-thinking organisations can use it as a catalyst for innovation and modernisation.

Cognizant is uniquely positioned to help banks navigate the complexities of the motor finance remediation challenge. Our end-to-end AI capabilities include:

- Data asset creation

Using gen AI to extract and consolidate data from unstructured sources, ensuring a complete and accurate view of customer agreements.

AI-assisted claims management

A plug-and-play solution that integrates with existing cloud environments (e.g., Azure, AWS) to handle the entire claims process, from multi-channel submissions to automated calculations and communications.

Regulatory expertise

Ensuring compliance with GDPR, Consumer Duty regulations, and responsible AI principles while safeguarding customer data.

Operational efficiency

Combining AI with human oversight to ensure accuracy and scalability, reducing the need for temporary staff and minimising costs.