Chris Allen, Cognizant’s Head of Retail Banking Consulting in the UK and Ireland, Graham McConney, AI Advisor and Talha Ghafoor, Senior Director UK and Ireland, explore how financial institutions can leverage cutting-edge AI and data management solutions to tackle the motor finance remediation crisis efficiently while restoring trust and ensuring compliance with FCA deadlines.

The motor finance industry is in the midst of an unprecedented remediation crisis. Discretionary Commission Arrangements (DCAs), where brokers added undisclosed interest to loans in exchange for commissions, were declared unlawful by the Court of Appeal in October 2024.

The Financial Conduct Authority (FCA) has mandated that firms resolve all DCA-related complaints by December 2025. Mishandling these claims risks severe regulatory penalties, reputational damage, and operational strain. However, financial institutions now have access to technologies that can revolutionise remediation. By using AI-driven solutions, they can ensure compliance while transforming their operations to meet future regulatory challenges more effectively.

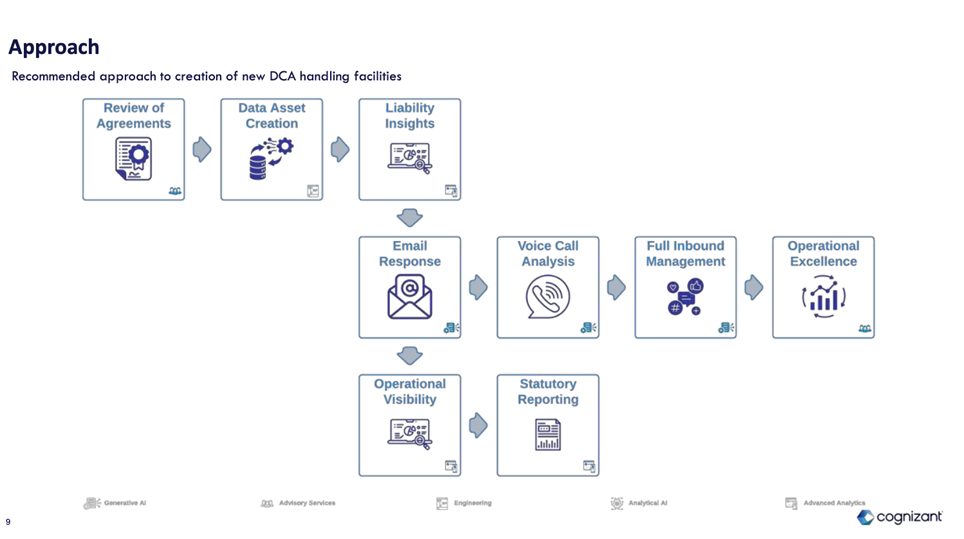

Financial institutions need a structured plan to handle the motor finance crisis efficiently. Cognizant recommends the following roadmap, which combines advanced data handling, AI tools, and streamlined operations.

1. Review of agreements

The first step is to gather and analyse historical agreements, many of which date back to 2007. This is a crucial yet challenging process, as much of this data is fragmented across legacy systems, paper archives, and unstructured formats like PDFs.

AI-driven solutions like Generative AI can automate extracting and validating key data points, including vehicle & driver details, loan values and interest rates. By consolidating this information, institutions can create a complete and accurate dataset, laying the groundwork for effective remediation.

2. Data asset creation

Once agreements are reviewed, the next step is to build a centralised "data asset". This repository integrates extracted data into a standardised format, allowing seamless workflows for redress calculations, customer communications, and compliance reporting.

AI enables this process to occur at scale, ensuring that even vast amounts of unstructured data can be organised efficiently. This consolidated view also helps institutions identify trends in their exposure, improving both prioritisation and decision-making.

3. Liability insights and redress calculations

With a robust data asset in place, financial institutions can leverage AI to calculate liabilities and determine redress amounts quickly and accurately. Unlike manual methods prone to inconsistencies, AI ensures transparency and compliance with FCA guidelines.

AI tools can also identify systemic patterns of overcharging, helping institutions to address broader issues while providing fair compensation to customers. By automating these calculations, banks can drastically reduce processing times and minimise the risk of errors.

4. Multi-channel email and voice call management

Effective communication is essential to restoring trust. AI-powered platforms can streamline interactions across email, phone calls, web portals, and apps, ensuring consistent messaging tailored to individual customers.

For instance, AI can analyse voice calls for sentiment and intent, helping institutions prioritise urgent cases. At the same time, automated email responses can provide timely updates, reducing frustration and improving customer satisfaction.

5. Full inbound management

It is vital to manage the influx of complaints. AI systems can triage and categorise claims, directing them to the appropriate workflows based on complexity and urgency. This ensures that high-priority cases are handled promptly while routine tasks are resolved efficiently.

By automating these processes, institutions can handle fluctuating complaint volumes without hiring large temporary workforces, reducing costs and operational strain.

6. Operational visibility and statutory reporting

Transparency is a cornerstone of FCA compliance. Modern remediation systems provide real-time visibility into the status of every claim, creating a detailed audit trail.

This operational insight also supports statutory reporting, enabling institutions to meet regulatory requirements while reducing the administrative burden on teams.

7. Achieving operational excellence

The final step is embedding scalability and resilience into remediation operations. By combining AI with human oversight, institutions can handle complex cases while automating routine tasks. This hybrid model ensures both speed and accuracy, enabling institutions to meet deadlines and exceed customer expectations.