Financial institutions face mounting pressure to transform their traditional operating models as consumers demand personalised, customer-first experiences over conventional products and services.

It's a Tuesday morning in 2030, and Sarah, a 25-year-old freelance graphic designer in Manchester, opens her smartphone to understand her financial health and options.

Five years earlier, she saw a simple account balance when opening one of her four banking apps, but now she's greeted by a personalised financial wellness dashboard embedded within the fabric of her phone's operating system. The service notices her irregular income patterns across all her accounts and suggests a flexible savings solution that automatically adjusts to her cash flow.

When Sarah mentions in an online chat that she's considering buying her first home, she isn't pushed a mortgage product. Instead, it creates a holistic "home-buying journey" that includes budgeting guidance, deposit-saving strategies, and educational content about the property market.

This capability isn't just a technical upgrade but a fundamental shift in how banks serve their customers. We're witnessing the transition from a product-centric model that has dominated for decades to one that genuinely puts customers at the heart of financial services. Welcome to the new world of banking.

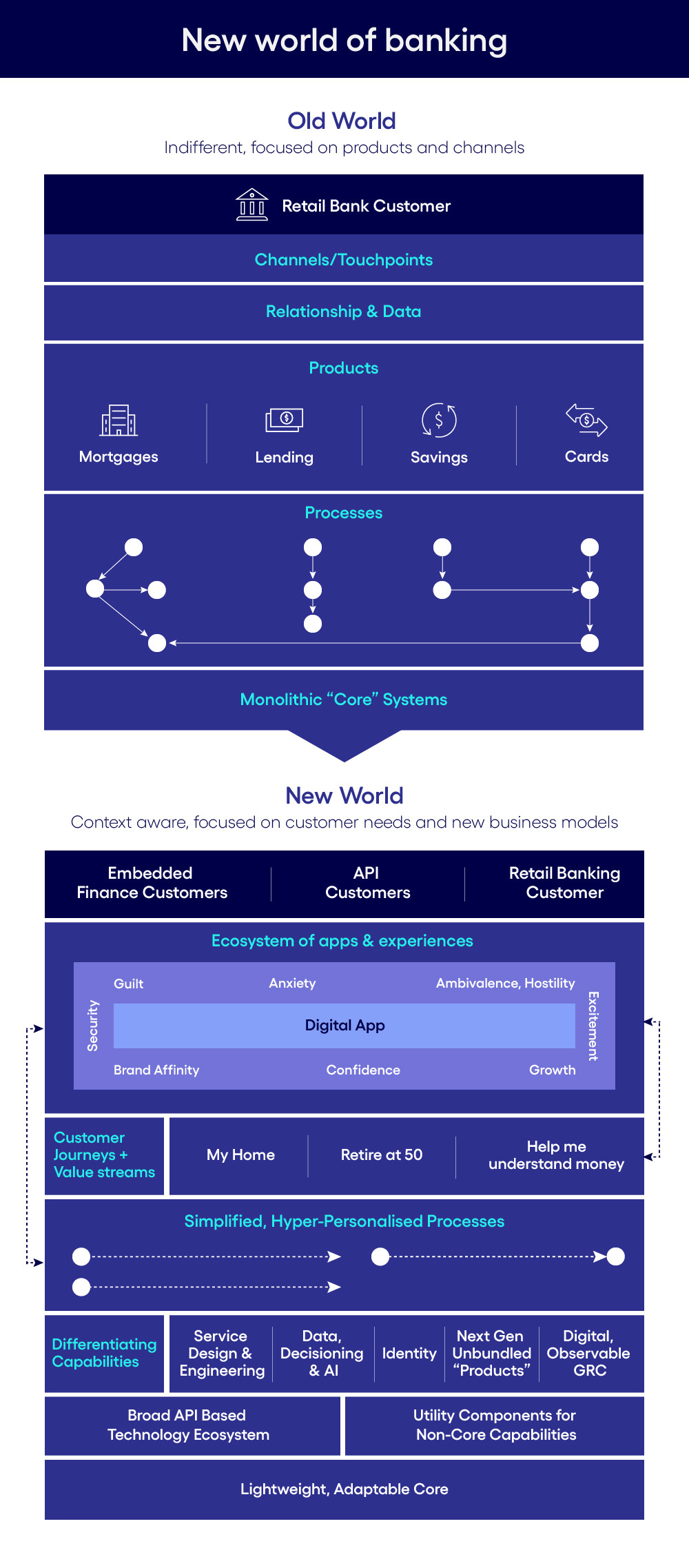

Move away from product-first banking

Traditional banking – the old world – was built around products and channels, not people. Banks operated in silos: mortgages, savings accounts, credit cards, and loans were treated as separate entities, each with their own rigid processes and success metrics.

Meanwhile, branch managers focused on product sales targets rather than customer outcomes. The infrastructure supporting this model – monolithic core banking systems – was as inflexible as the thinking behind it.

This approach must align more with modern customer expectations in the digital age. New Cognizant research shows that 79% of customers want their providers to help them save against their life goals, such as getting married or buying a house. Yet most savings accounts don't help people save – they simply store money.

Similarly, 63% of customers want their provider to switch products on their behalf to secure better rates proactively, but traditional banks often profit from customer inertia.

The disconnect is particularly stark in how banks handle financial difficulties. When customers face challenges, banks are usually the last institution they turn to for help despite being best positioned to offer support. This trust deficit stems from decades of prioritising products over people.

Context-aware banking

The emerging banking model is built around customer context and life moments. Instead of pushing products, banks are beginning to organise themselves around customer journeys: "helping me buy a home" rather than "selling me a mortgage", for instance, or "supporting my business growth" rather than "providing a business loan".

This shift is enabled by technology but driven by changing customer expectations. Modern banking platforms use APIs and microservices to create flexible, personalised experiences. They can adapt processes in real time based on customer circumstances and preferences. More importantly, they're designed to support continuous engagement rather than transactional relationships.

Demographic shifts underscore the urgency for this transformation. By 2030, Generation Z will represent 30% of the global population. Our data shows a clear generational divide in banking preferences: while older customers prioritise interest rates and traditional product features, younger consumers place greater value on user experience, brand alignment, and emotional engagement with their financial services providers.

This younger cohort doesn't just want different features; they want a different relationship with money altogether. They expect their financial institutions to be partners in their economic well-being, offering proactive guidance and seamless integration with their digital lives.

Bridging the gap

The path from the old world to the new requires fundamental changes in three areas, outlined below.

1. Organisational structure and operating model

Banks must shift from product-based functions to teams that are more aligned with customer value. Instead of a "head of mortgages", we're seeing roles like "head of home buying" or "head of lifetime savings" become commonplace. Of course, recruiting new leadership or changing titles of existing talent is the easy bit; ensuring the operating model of the organisation can support new focus will be the area of most challenge.

2. Technology architecture

The transition from monolithic systems to flexible, API-driven platforms isn't just a technical upgrade. It's a prerequisite for delivering personalised, context-aware services at scale. When examining the business case for these types of changes, it can be useful to consider the additional opportunities they present beyond a bank's existing product-led construct.

3. Cultural transformation

Perhaps the most challenging is the shift in mindset from selling products to solving problems. This change requires new metrics that measure customer outcomes rather than just product sales. While traditional KPIs focusing on underlying financial products will remain, forward-looking organisations will pair these with measures focused on delivering broader customer needs – such as financial understanding, and brand affinity, and so on.

4. Know your customer

Most banks are currently configured around the premise that they design, distribute and service products for customers that they "own". In the new world, banks will need to become increasingly comfortable with distributing an API or embedded finance product for others to sell and service.

Some traditional banks are already making progress. We're seeing the emergence of "lifestyle banking" apps that integrate financial services with customers' broader life goals. However, the gap between customer expectations and current capabilities remains substantial.

Trust is a must

The future of banking will be defined by how well institutions can embed themselves into customers' lives as trusted partners rather than just service providers. Success will come to those who can combine the trust and stability of traditional banking with the customer-centricity and technological capability of fintech innovators.

For established banks, this transformation isn't optional. Our research shows that even older customers are increasingly drawn to providers who can genuinely understand their needs and circumstances. The question, then, isn't whether to change but how quickly institutions can adapt to this new reality.

The winners won't be those with the best products but those who best understand and serve their customers' needs. The measure of success will shift from product penetration to customer outcomes and how effectively banks help their customers set and achieve their financial goals.

The shift from the old to the new world of banking isn't about better products or faster technology. Ultimately, it's about finally putting customers where they always should have been: at the heart of every decision, every service, and every interaction.