Gen AI adoption in the Nordics: Balancing ambition with caution

Written by Stig Martin Fiskå & Duncan Roberts

3rd October 2024

Nordic businesses are keeping pace with global generative AI investment trends, with average projected spending reaching $49.7 million per company this year, according to our recent research, slightly above the global average of $47 million.

These investments are taking place amid a sense of urgency to realize the potential of this powerful technology, with 65% of businesses expressing a desire to accelerate their generative AI strategies. At the same time, about two-thirds (62%) of Nordic businesses express at least moderate worry about the existential impact of generative AI on their operations.

This measured perspective is perhaps characteristic of a region known for its thoughtful approach to pursuing technological advancement within the context of its potential societal and ethical implications, as seen in its early investment into sustainability.

To better understand what generative AI adoption will look like globally, we conducted a study of 2,200 business leaders in 23 countries and 15 industries, including 110 in the Nordics. The study assessed a wide range of generative AI adoption trends, including investment levels, use cases, how critical gen AI strategies are to business success, and organizational readiness to adopt the technology.

We also analyzed 18 regional and internal business factors that will either inhibit or accelerate business adoption of gen AI (see the end of the report for the full list of factors). Respondents evaluated each factor’s potential impact on their generative AI strategy, rating it as either positive or negative on a scale of high to low impact.

From the results, we calculated a “momentum score” for each country or region. The momentum score represents the level of confidence business leaders have about being able to roll out their generative AI strategy based on internal business factors and the prevailing local conditions of their country or region.

For all the regions covered, inhibitors to adoption outranked accelerators, meaning that all momentum scores skewed negative. In effect, businesses globally feel constrained by their operating environment.

But to understand how different regions varied relative to each other, we averaged the ratings to establish a baseline global momentum score. This approach enabled us to identify regions that are more optimistic about their ability to adopt the technology compared with a global average.

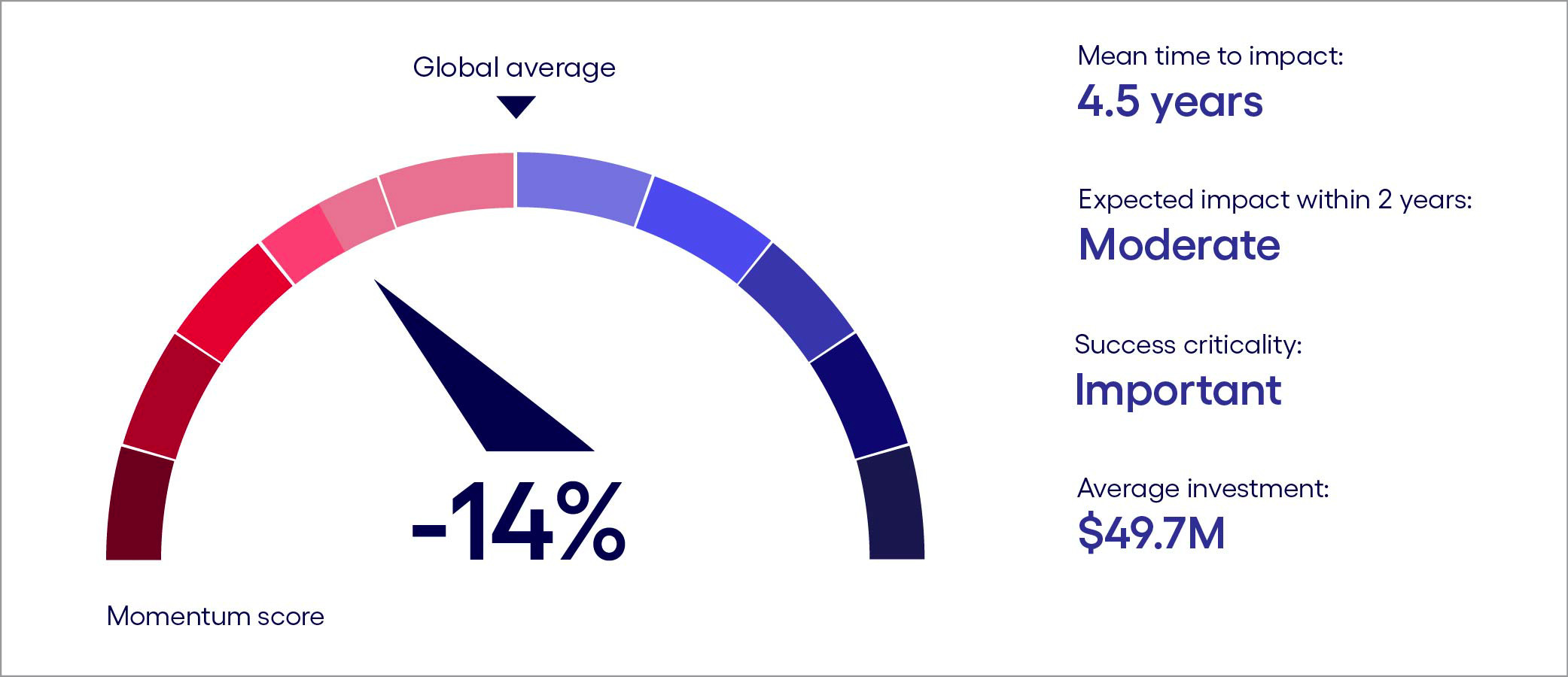

While there is clear investment in generative AI across the Nordic region, the overall momentum score of -14% indicates a more cautious approach compared with the global average. Several factors contribute to this measured pace, notably concerns surrounding consumer perceptions, the adaptability of existing business models, and the cost and availability of skilled talent. Additionally, challenges related to current technology infrastructure and the perceived maturity of generative AI technologies are contributing factors.

However, Nordic businesses display a more optimistic outlook in key areas. They express greater confidence in their operating models' flexibility, market demand, the quality of generative AI outputs, data readiness and the availability of compute power. This suggests that companies will be able to leverage internal strengths to address specific challenges and accelerate their adoption of generative AI.

Nordics gen AI scorecard

Base: 110 senior business leaders in the Nordics

Source: Cognizant and Oxford Economics

Figure 1

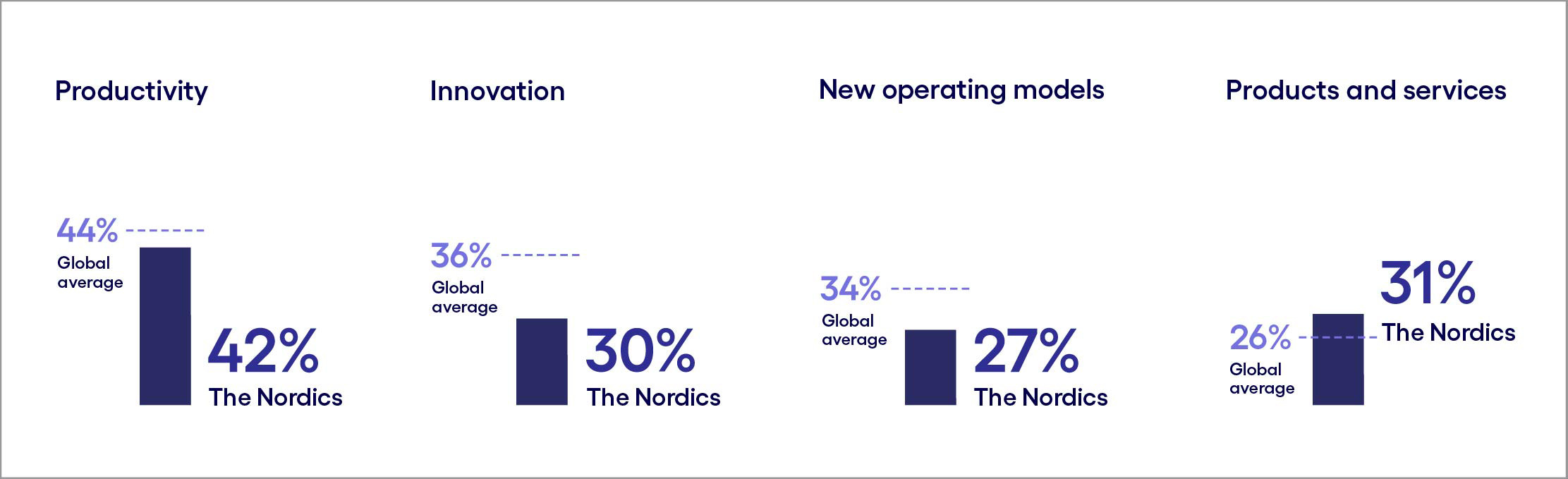

As for where businesses’ generative AI investments will be aimed in the near term, we looked at two distinct uses of the technology: productivity, such as helping people work more quickly and get more done, and disruptive innovation, which involves more sweeping change to business and operating models. Overall, businesses in the Nordics mirror the global trend: Over the next two years, more respondents expect to use generative AI to boost productivity than drive disruptive change (see Figure 2).

However, our study also reveals a change in what productivity means when pursued with generative AI. The end goal is not efficiency and cost-cutting as has been the case with previous automation endeavors. This new dynamic requires fresh thinking around understanding business use cases of generative AI, which we’ll address later in this report.

Notably, Nordic businesses are more likely than their global peers to embed generative AI into their products and services in the next two years (31% vs. the global average of 26%). This suggests a pervasive belief that generative AI will become an integral part of the Nordic business landscape and citizens’ digital lives.

Greater focus on productivity than innovation

Q: Which of the following best describes the role generative AI will play in your organization's business strategy in the next two years? (Percent of respondents naming each as a top-3 choice)

Base: 110 senior business leaders in the Nordics

Source: Cognizant and Oxford Economics

Figure 2

This report identifies the regional and business factors that could either inhibit or accelerate generative AI momentum in the Nordics. It also provides an industry-specific look at how generative AI will be used, a regional focus on business readiness, and strategies for Nordic businesses to successfully implement generative AI.

Inhibitors and accelerators: The forces driving AI momentum

To dig deeper into these mechanics, rather than comparing to a global average, we’ll now examine how business leaders rate inhibitors and accelerators within their region. By doing so, our study provides a detailed temperature check on what respondents view as the main inhibitors and accelerators to generative AI in their region.

With this assessment, leaders can take advantage of what’s working well in their local environment, while strategizing on overcoming challenges.

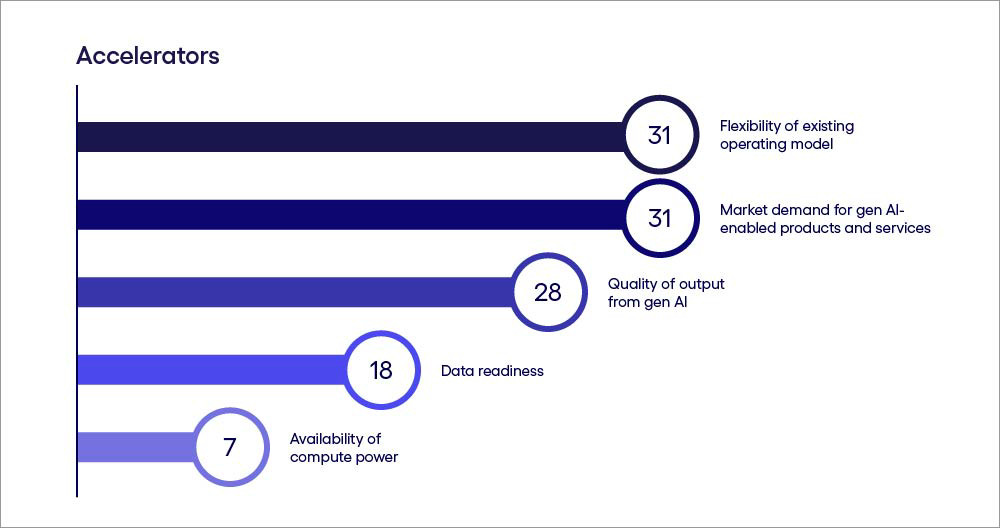

A look at Nordic gen AI accelerators

Respondents were asked which factors inhibit or accelerate their organization's adoption of generative AI. Score represents a percentage point difference to the country's momentum score compared to the global baseline.

Base: 110 senior business leaders in the Nordics

Source: Cognizant and Oxford Economics

Figure 3

The flexibility of operating models in Nordic companies serves as a strong foundation for generative AI adoption. Companies like Danish shipping and logistics giant Maersk, for example, have successfully integrated AI into their operations to track shipments, anticipate disruptions and proactively identify alternatives.

Complementing this adaptability is a growing market demand for generative AI. AI tool usage is widespread in the Nordic region, with nearly half the population using these tools to some extent in 2024. This underscores the need to invest in and enhance the region's infrastructure to match changing behaviors and enhance safe and effective use.

Data readiness further bolsters the region's prospects. In many ways, the Nordic region is leading the charge on data issues, especially as it relates to privacy. For example, Finland's "MyData" initiative, which enables people to own and control the use of their personal data, exemplifies the Nordics' commitment to data management, privacy and security, and provides a strong foundation for safer development and deployment of generative AI applications.

At the same time, a significant portion (48%) of businesses believe their data security practices are not robust enough to support generative AI initiatives. This highlights the need for investment in modernizing infrastructure and strengthening security measures to ensure the responsible and safe deployment of AI technologies.

Finally, the availability of compute power also plays a significant role. The presence of major data centers from global cloud providers and initiatives like the LUMI petascale supercomputer in Finland ensures that Nordic businesses have access to the computational resources necessary for generative AI development.

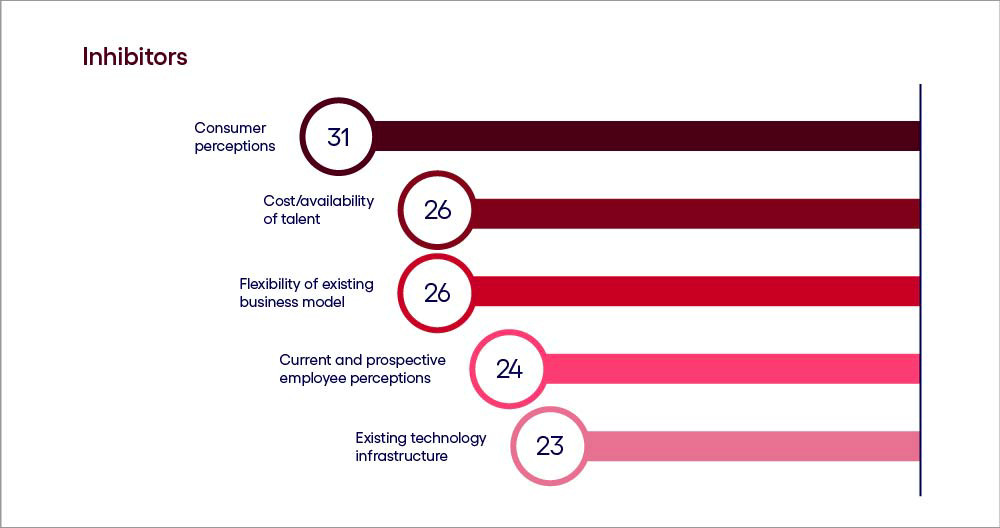

Understanding Nordic gen AI inhibitors

Respondents were asked which factors inhibit or accelerate their organization's adoption of generative AI. Score represents a percentage point difference to the country's momentum score compared to the global baseline.

Base: 110 senior business leaders in the Nordics

Source: Cognizant and Oxford Economics

Figure 4

While the Nordics demonstrate a promising outlook on certain aspects of generative AI adoption, several challenges persist, dampening overall momentum in the region.

Consumer perception tops the list of inhibitors to scaled adoption in the Nordics, which is understandable given the various ethical, regulatory and privacy concerns that surround the technology. While a majority of respondents (74%) say they are experimenting with customer-facing use cases of generative AI, 46% are not confident about their existing technology’s ability to support compliance with customer privacy regulations. This underscores the need for businesses in the region to build trust and transparency with the public.

The global scarcity of AI talent is another pressing concern. While 30% of businesses plan to hire to fill knowledge gaps, our research indicates significant apprehension among companies regarding talent acquisition. This concern is likely exacerbated by the competitive talent market, particularly for high-demand roles, such as data scientists, data engineers and machine learning engineers. Relying solely on external hires may not be a sustainable long-term strategy, prompting 491% of businesses to rely on training programs for existing employees in generative AI and 26% to consider external partnerships to bridge skills gaps.

The Nordic region is home to innovative initiatives such as AI Labs in Sweden, which aims to address both talent and infrastructure challenges. However, the persistent scarcity of AI talent underscores the urgency for businesses to develop comprehensive strategies that encompass both talent acquisition and development.

Sector spotlight: Stark differences in industries’ gen AI adoption priorities

Of course, there are many use cases and strategies for using generative AI. As we’ve said, Nordic businesses are primarily focused on realizing productivity gains with generative AI, at least in the next two years. However, a look at what’s driving their business cases sheds a new light on productivity from how it’s been seen historically.

Traditionally, businesses have equated automation productivity gains with cost-cutting: driving down the cost of output by reducing the number of people needed to get work done.

While generative AI-driven automation will likely lower headcount to some degree, that is no longer the end goal. Instead, as seen through the metrics respondents will use to drive business cases, we see a shift toward redirecting productivity gains into funding endeavors that increase revenues or lead to entirely new revenue streams.

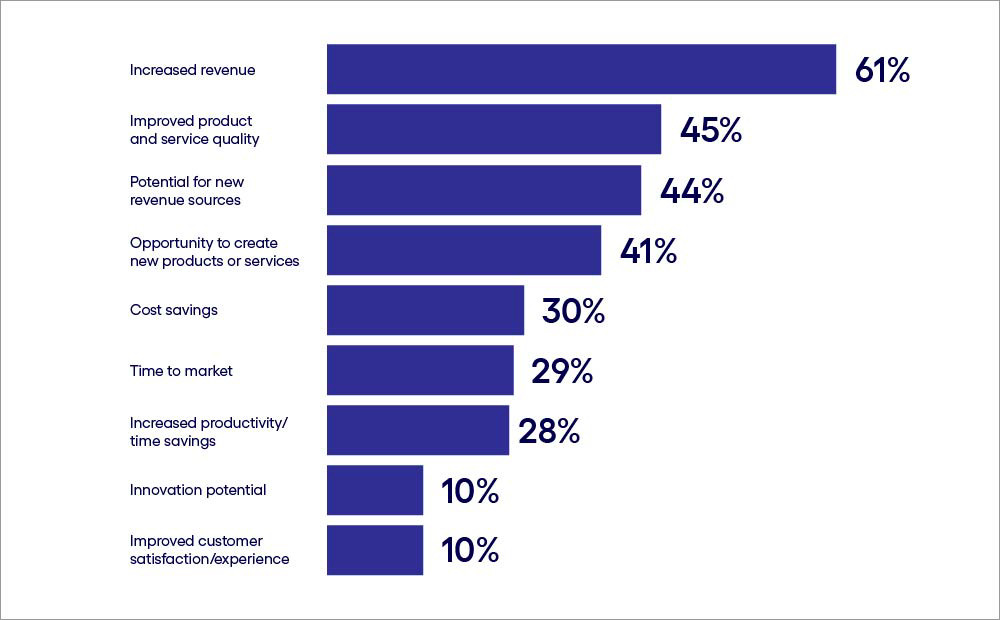

The metrics Nordic businesses say will be most important for justifying generative AI expenditures include increasing revenues, discovering new revenue sources and improved product and service quality, all of which were named by at least 44% of respondents (see Figure 5). Conversely, metrics like cost savings, time-to-market and productivity were cited by less than 30% of respondents. In other words, the concept of productivity no longer stops at cost-cutting—businesses appear to be redirecting productivity gains into initiatives aimed at growth.

This emphasis on growth-oriented metrics also reflects the unique socioeconomic landscape of the Nordics, which discourages workforce reductions. Further, strong labor unions can make such measures costly, particularly for larger enterprises. Consequently, these businesses tend to favor strategies that empower them to achieve "more with the same" rather than pursuing the traditional "same with less" approach.

Revenue is a top metric for justifying gen AI use cases

Q: Which of the following metrics are most important in terms of justifying your organization’s generative AI business cases? (Percent of respondents naming each as a top-three choice)

Base: 110 senior business leaders in the Nordics

Source: Cognizant and Oxford Economics

Figure 5

Using this more granular view of productivity goals and business drivers, we analyzed the differences in how industries intend to use the technology.

Rather than focusing on the distinction between productivity vs. innovation, we grouped the metrics into two high-level categories of business use cases:

- Enhancing current business performance (revenue, cost savings, time-to-market, productivity)

- Building something new (new revenue sources, new or improved products, innovation)

We then assigned each of the metrics a score to see the relative gap between a number-one-ranking metric and a number-three-ranking metric. By calculating the average score across industries, we could clearly see how each industry’s responses deviated from the baseline.

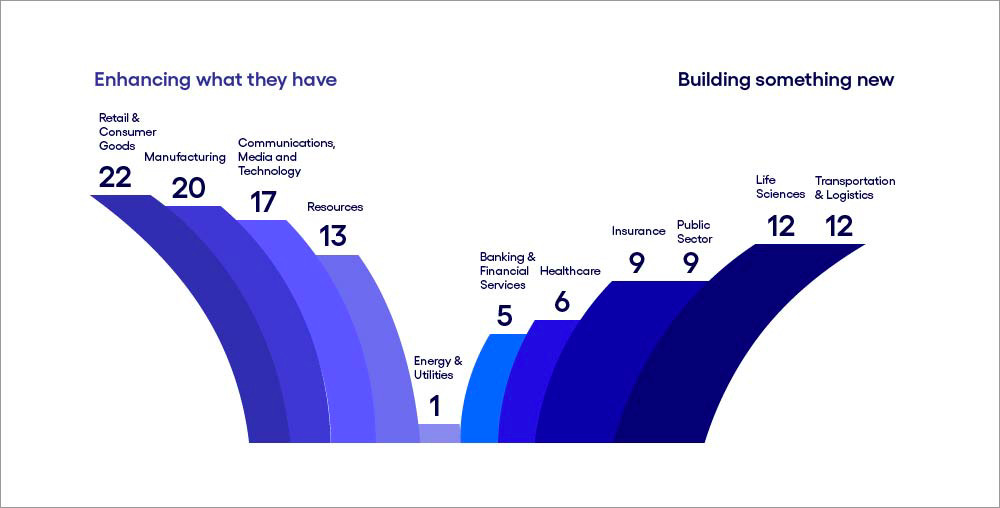

Our analysis reveals stark differences among Nordic industries in terms of the business use cases they’ll likely prioritize (see Figure 6).

Industries diverge on business cases

Note: This figure depicts each industry’s relative deviation from a baseline of “zero,” using a ranked scoring of the top-three metrics respondents cite as important for justifying their generative AI use cases. It reveals a weighted view of each industry’s overall priorities for gen AI deployment.

Base: 110 senior business leaders in the Nordics

Source: Cognizant and Oxford Economics

Figure 6

Retail and consumer goods: Retail giants like IKEA are harnessing the power of generative AI to reshape the customer journey. The retailer released an AI-powered design assistant, enabling customers to experiment with different furniture arrangements and styles using natural language prompts. This not only empowers customers to visualize their dream spaces, but also demonstrates IKEA's commitment to innovation and customer-centricity.

Communications, media and technology: Spotify, the Swedish audio streaming powerhouse, exemplifies the Nordics' leadership in leveraging generative AI for innovation. Spotify's recently launched AI Playlist feature empowers users to create highly personalized playlists simply by typing in a descriptive prompt. Whether it's "upbeat pop songs for a summer road trip" or "ambient music for coding," Spotify's generative AI translates these prompts into unique and tailored listening experiences, setting a new standard for music discovery and personalization.

Healthcare: Nordic countries are known for their universal healthcare system, and generative AI is being seen as one way to increase efficiency and reduce costs while also improving care. In Finland, the Helsinki University Hospital is piloting an AI-powered medical transcription service that converts doctors' spoken notes into accurate and structured medical records. This significantly reduces administrative burden, enabling healthcare professionals to focus more time on patient care.

Insurance: The insurance sector in the Nordics is leveraging generative AI to streamline processes and enhance customer experiences. For instance, the Danish insurance company Tryg is using AI-powered chatbots to handle customer inquiries and claims processing, resulting in faster response times and improved customer satisfaction. Generative AI is also being used to analyze vast amounts of data to identify fraud patterns and assess risk more accurately, leading to more efficient underwriting and claims management processes.

Business constraints to gen AI adoption: Talent and tech infrastructure

A remaining question is whether businesses are ready to drive real value from these use cases.

The answer, according to our research, is mixed. To better understand how prepared executives believe their business is to adopt generative AI, we asked respondents to rank their organization’s maturity on a scale of 1 to 4 by selecting a statement that best described their organization in the following five areas, from low maturity to high:

- Organizational agility

- Leadership commitment

- Skills and talent

- Strategy and approach

- Technology and infrastructure

The output reveals where business leaders believe they are already mature, and areas where they feel the need to evolve capabilities considerably to make generative AI investments work.

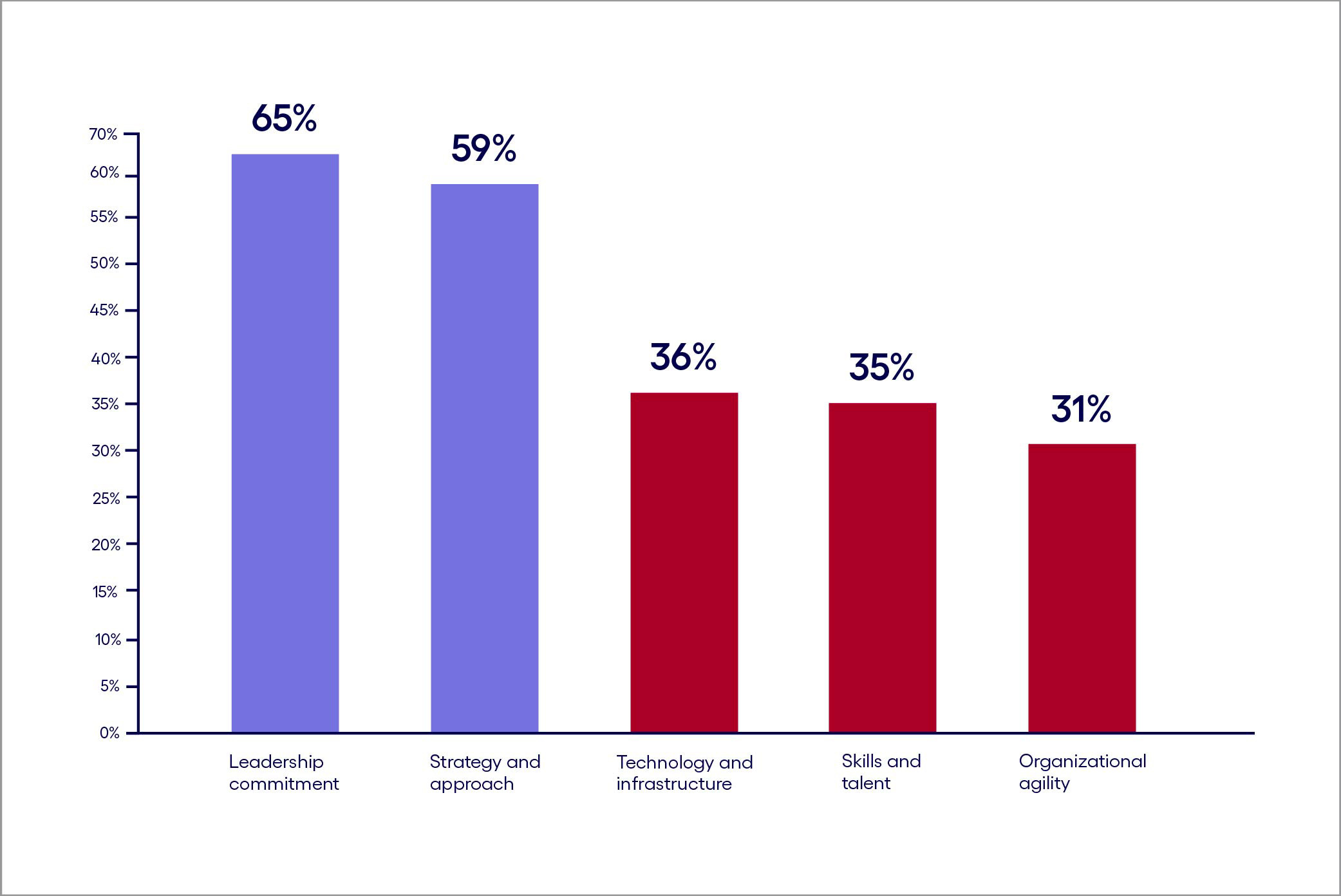

Leadership support is sound, but fundamentals are lacking

Respondents were asked to rate the maturity of their organization's operations in relation to generative AI. (Percent of respondents rating each as a 3 or 4, with 4 representing the highest level of maturity).

Base: 110 senior business leaders in the Nordics

Source: Cognizant and Oxford Economics

Figure 7

Nordic respondents present a nuanced view of their readiness for generative AI. While the majority of respondents rated leadership commitment and strategy as mature or highly mature, foundational elements like technology infrastructure, skills and organizational agility need strengthening (see Figure 7).

A particular area of concern is skills and talent as the skills gap could hamper the successful implementation and utilization of generative AI technologies. Moreover, the low ratings for technology and infrastructure highlights potential challenges in data management, processing capabilities and overall technological preparedness for the demands of generative AI.

Nordic organizations also grapple with data accessibility issues. Although 52% believe their data is in good condition, a mere 22% rate their data accessibility as good or excellent. This discrepancy underscores the challenge of harnessing data effectively for generative AI applications, which demands not only clean data but also readily available information across business units and stakeholders.

It is particularly worrying that 45% of Nordic respondents anticipate their compliance with generative AI government regulations will be either nonexistent or inadequate. This is especially concerning given the Nordic region's strong emphasis on regulation and social welfare.

Path to success: Strategic recommendations for Nordic businesses

To fully capitalize on the potential of generative AI and overcome existing challenges, Nordic businesses should prioritize the following actions:

- Upskill and empower the workforce: To address a growing skills gap in AI and other digital areas, companies will need to prioritize retraining and upskilling existing staff in generative AI. This will foster a workforce capable of effectively leveraging AI technologies, maximizing their potential for innovation and productivity. For example, Elements of AI is a series of open online courses sponsored by the Icelandic government as a way to strengthen the knowledge of AI among Iceland citizens.

- Prioritize data accessibility: Companies can bridge the gap between data quality and usability by investing in robust data management solutions. Ensure data is not only clean and reliable but also readily accessible for AI algorithms, empowering informed decision-making and innovation.

- Build customer trust and awareness: Companies must recognize the critical role of consumer perception in AI adoption. Focus on building trust and transparency by clearly communicating how AI is being used and its benefits and addressing concerns about accuracy and ethical implications. Companies must also take steps to ensure consumer data privacy and security standards are upheld.

- Foster collaboration and innovation: Leverage the Nordic region's strong innovation ecosystem by fostering collaboration between established businesses and startups. This will provide access to specialized AI expertise and fresh perspectives, enabling businesses to overcome the skills gap and accelerate AI adoption.

- Balance leadership enthusiasm with measurable results: While leadership commitment is strong, ensure that AI initiatives are grounded in practical use cases and pilot projects that deliver tangible business value. This will foster a culture of experimentation and learning, driving sustainable AI adoption.

*The full list of regional factors we evaluated includes: the flexibility of the existing operating model, market demand for gen AI-enabled products and services, data readiness, quality of output from gen AI, availability of compute power, cost/availability of gen AI-related technologies, shareholder/investor sentiment, regulatory environment, sustainability, national infrastructure, cost/availability of capital, data privacy and security, existing technology infrastructure, current and prospective employee perceptions, flexibility of the existing business model, maturity of gen AI-related technologies, consumer perceptions and cost/availability of talent.

Learn about the impact of generative AI on jobs and the economy in our report New work, new world.